黄金科学技术 ›› 2021, Vol. 29 ›› Issue (4): 510-524.doi: 10.11872/j.issn.1005-2518.2021.04.194

郑明贵1,2( ),曹天琦1(),曾健林1

),曹天琦1(),曾健林1

Minggui ZHENG1,2(),Tianqi CAO1(),Jianlin ZENG1

摘要:

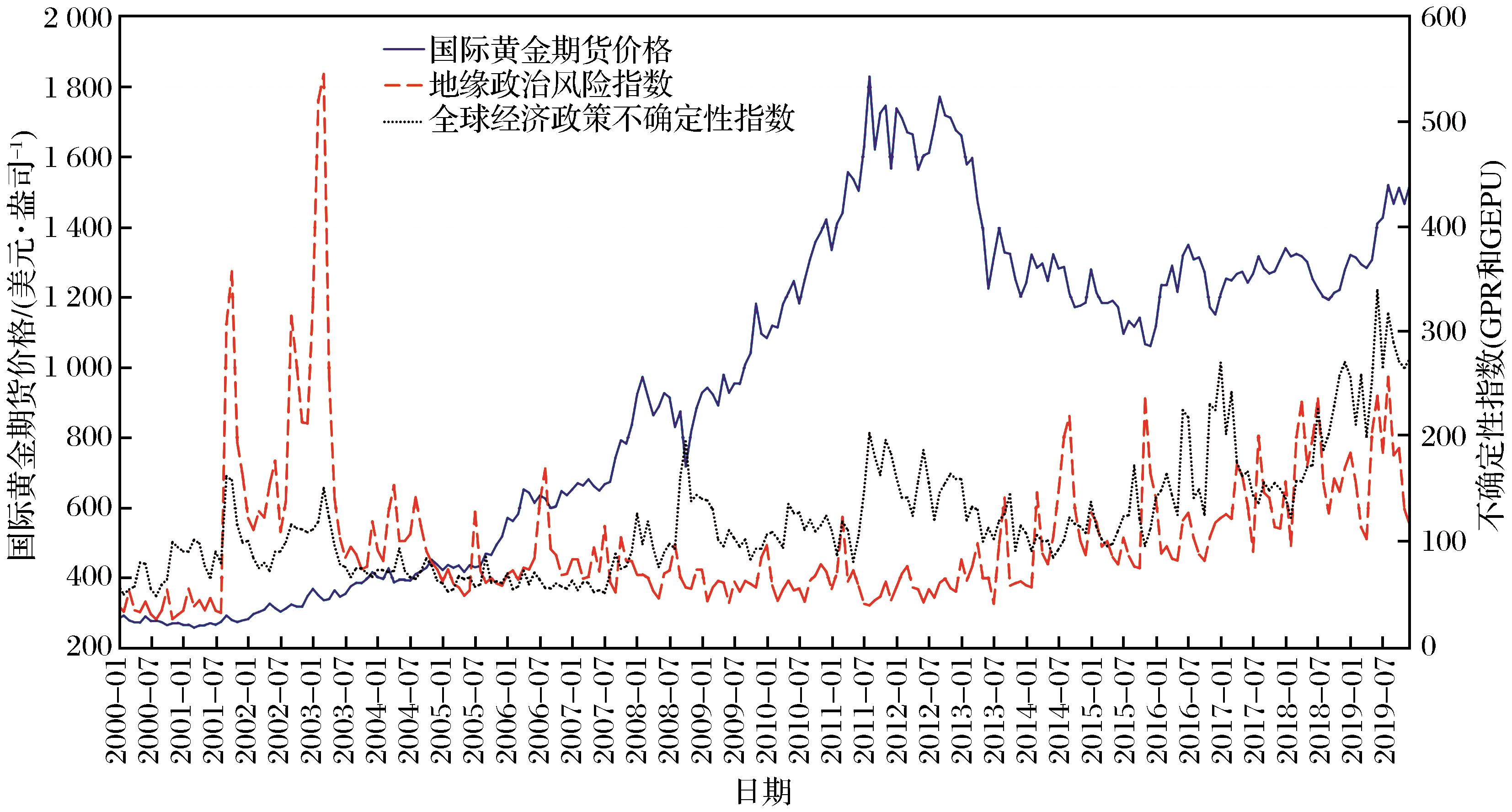

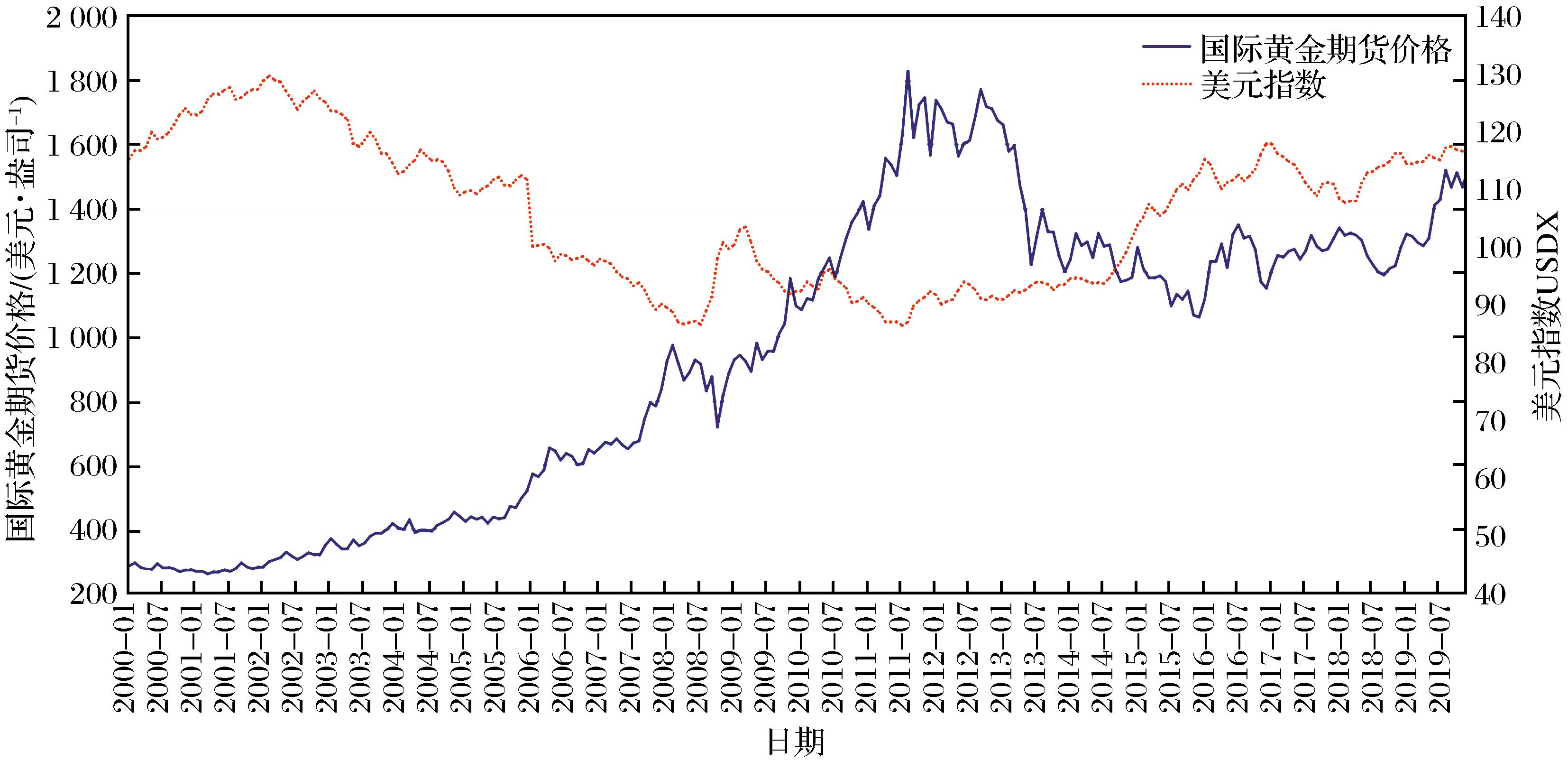

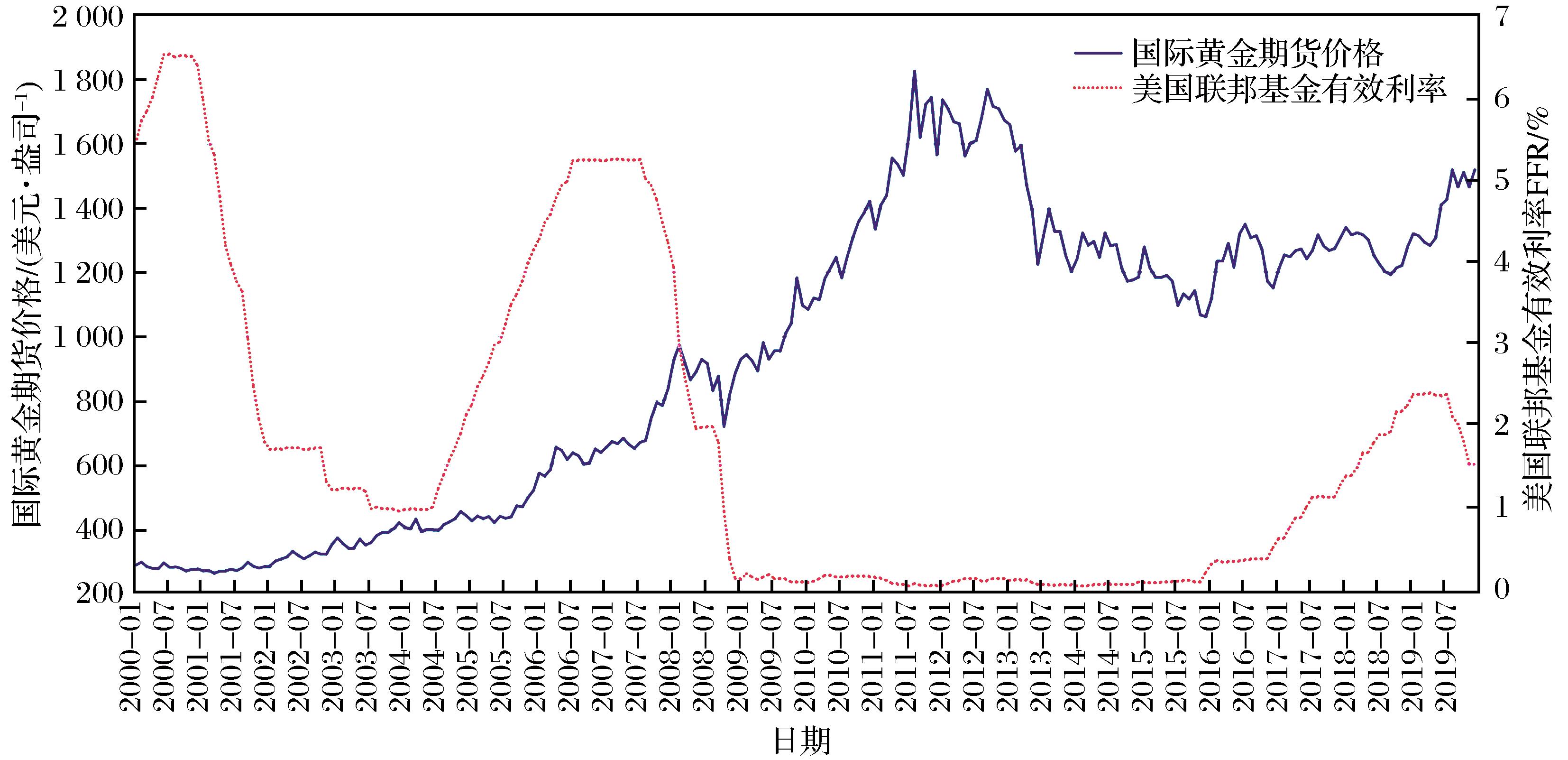

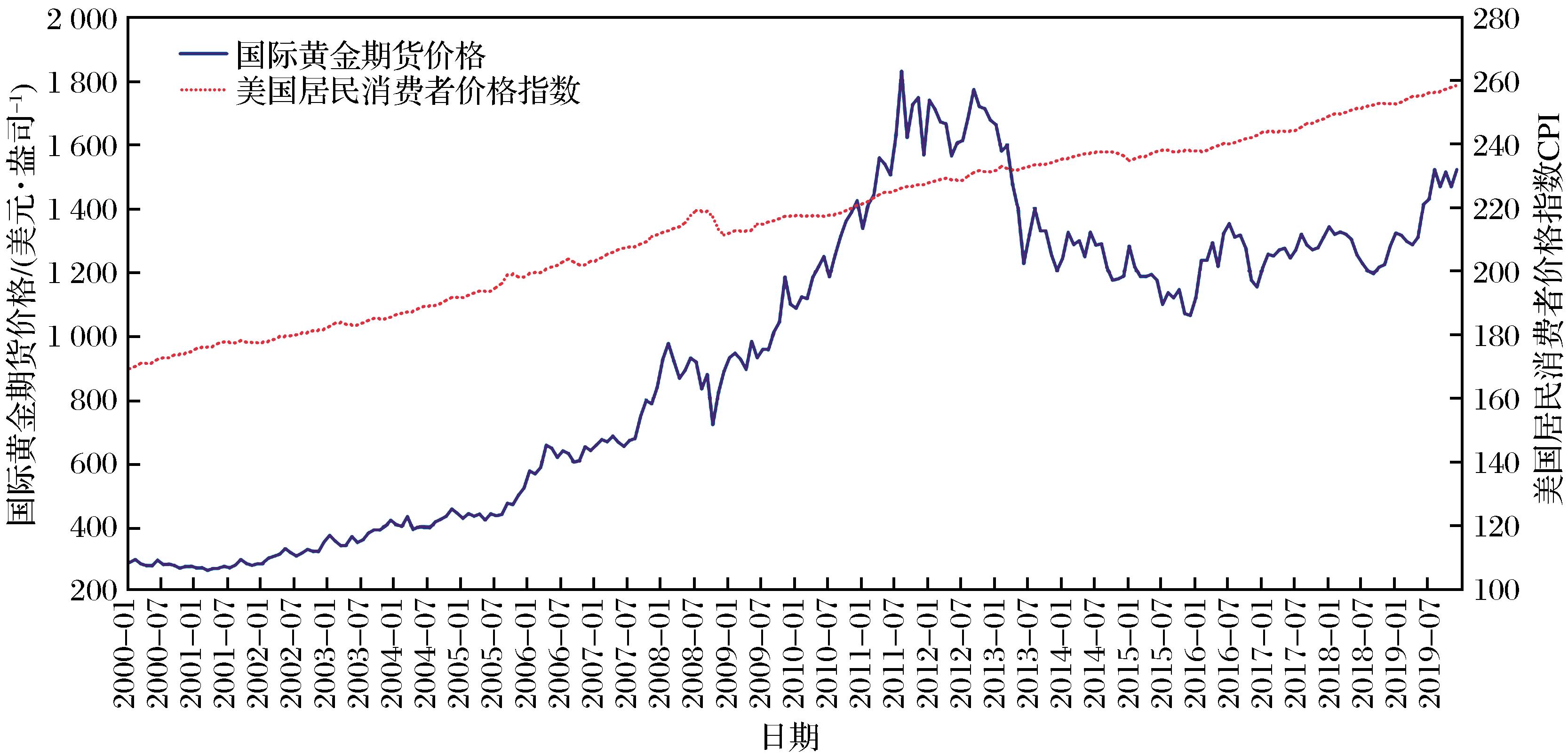

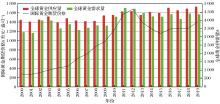

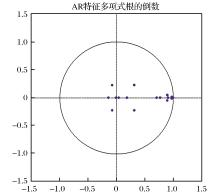

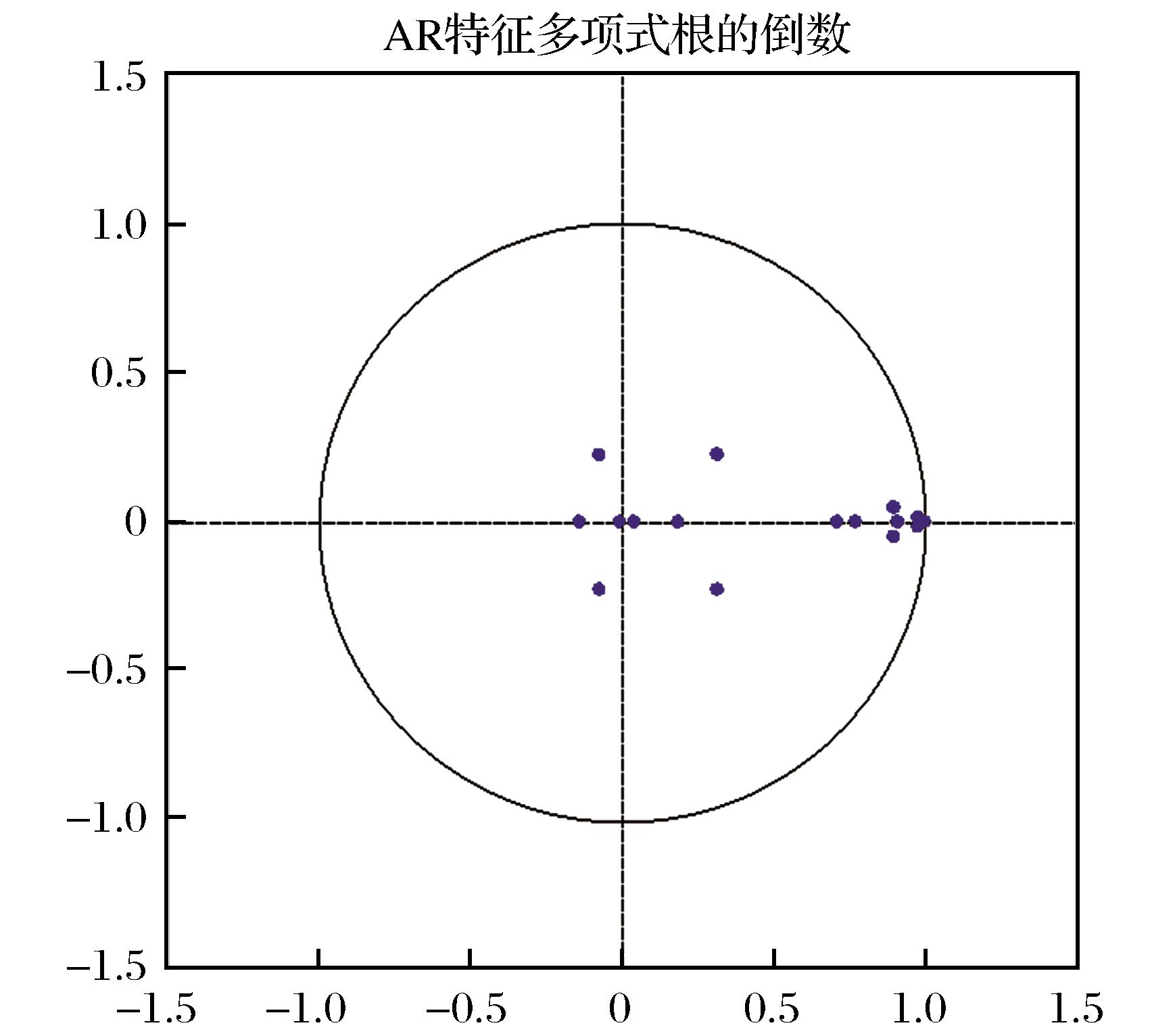

全球政治经济环境的不稳定性会造成国际黄金期货价格的剧烈波动。为探究国际黄金期货价格的主要影响因素,利用2000—2019年国际黄金期货月度价格数据,运用向量自回归(VAR)模型、向量误差修正(VECM)模型、协整检验、脉冲响应和方差分解进行实证研究。结果表明:国际黄金期货价格与地缘政治风险、经济政策不确定性、美元指数、利率水平、美国通货膨胀水平和全球黄金供需差值存在长期均衡关系,并且美国通货膨胀水平和美元指数对国际黄金期货价格影响最为显著。地缘政治风险和经济政策不确定性在短期内对国际黄金期货价格产生正向冲击,同时经济政策不确定性的正向影响周期更长。

中图分类号:

| Algieri B,Leccadito A,2019.Price volatility and speculative activities in futures commodity markets:A combination of combinations of p-values test[J].Journal of Commodity Markets,(13):40-54. | |

| Balcilar M,Gupta R,Pierdzioch C,al et,2016.Does uncertainty move the gold price?New evidence from a nonparametric causality-in-quantiles test[J].Resources Policy,49:74-80. | |

| Batten J A,Ciner C,Lucey B M,al et,2010.The macroeconomic determinants of volatility in precious metals markets[J].Resources Policy,35:65-71. | |

| Bilgin M,Gozgor G,Lau C,al et,2018.The effects of uncertainty measures on the price of gold[J].International Review of Financial Analysis,58:1-7. | |

|

Caldara D,Iacoviello M,2018.Measuring geopolitical risk[J].Social Science Research Network,(1222):1-66.DOI:10.17016/IFDP.2018.1222.

doi: 10.17016/IFDP.2018.1222 |

|

| Chen Yanyan,2018.A review of political uncertainty and corporate behavior[J].Communication of Finance and Accounting,(6):116-123,129. | |

| Chirwa T G,Odhiambo N M,2020.Determinants of gold price movements:An empirical investigation in the presence of multiple structural breaks[J].Resources Policy,69:101 818. | |

| Davis S J,2016.An index of global economic policy uncertainty[R].New York:NBER Working Papers. | |

| Erb C B,Harvey C R,2013.The golden dilemma[J].Financial Analysts Journal,69(4):10-42. | |

| Fang L B,Yu H H,Xiao W,al et,2018.Forecasting gold futures market volatility using macroeconomic variables in the United States[J].Economic Modelling,72:249-259. | |

| Feng Hui,Zhang Shulin,2012.Empirical analysis of determinants of international gold futures price[J].Chinese Journal of Management Science,20(Supp.1):424-428. | |

| Feng Yuyao,Liu Chang,Sun Xiaolei,2020.Measurement of interaction between uncertainty and crude oil market:A multi-scale methodology based on comprehensive integration[J].Management Review,32(7):29-40. | |

| Gao Fei,Gu Weiyu,2018.An analysis on the influencing factors of international gold price:Perspective of the dual nature of gold as a commodity and as a value guarantee[J].China Soft Science,(5):160-170. | |

| Hayo B,Kutan A M,Neuenkirch M,2012.Communication matters:US monetary policy and commodity price volatility[J].Economics Letters,(1):247-249. | |

| Hossein H,Sirimal S M,Rangan G,al et,2015.Forecasting the price of gold[J].Applied Economics,47(39):4141-4152. | |

| Hu Entong,2005.Dual attributes of gold and its price determination mechanism[J].Gold Science and Technology,13(5):1-7. | |

| Hua Jian,Liu Chenjun,2010.The change of gold price from the perspective of supply and demand[J].Finance and Economics,(12):30-33. | |

| Huang Guoxuan,2019.An empirical study on the function of price discovery in China’s gold futures market[J].Price:Theory&Practice,(9):92-95. | |

| Jegadeesh N,Titman S,1993.Returns to buying winners and selling losers:Implications for stock market efficiency[J].Journal of Finance,48(1):65-91. | |

| Kanjilal K,Ghosh S,2014.Income and price elasticity of gold import demand in India:Empirical evidence from threshold and ARDL bounds test cointegration[J].Resources Policy,41:135-142. | |

| Koop G,Pesaran M H,Potter S M,al et,1996.Impulse response analysis in nonlinear multivariate models[J].Journal of Econometrics,74(1):119-147. | |

| Levin E J,Wright R E,2006.Short-run and long-run determinants of the price of gold[R].London:World Gold Council. | |

| Li Y L,Huang J B,Chen J Y,2020.Dynamic spillovers of geopolitical risks and gold prices:New evidence from 18 emerging economies[J].Resources Policy,70:101938. | |

| Liu Haoran,2007.Analysis of factors influencing gold price and investment strategy[J].Price:Theory&Practice,(10):57-58. | |

| Liu Jie,2017.Oil and gold price linkage analysis[J].Gold,38(2):5-7 ,14. | |

| Liu Shuguang,Hu Zaiyong,2008.Stability analysis of long-term determinants of gold price[J].World Economy Studies,12(2):35-41,87. | |

| Lu Guoqing,Li Mingxue,2017.Research on the linkage between US dollar index and gold price[J].Price:Theory&Practice,(5):109-112. | |

| Mayer H,Rathgeber A W,Wanner M,al et,2017.Financialization of metal markets:Does futures trading influence spot prices and volatility?[J].Resources Policy,53:300-316. | |

| Mellios C,Six P,Lai A N,al et,2016.Dynamic speculation and hedging in commodity futures markets with a stochastic convenience yield[J].European Journal of Operational Research,250(2):493-504. | |

| Mensiab W,Sensoyc A,Vinh Vo X,al et,2020.Impact of COVID-19 outbreak on asymmetric multifractality of gold and oil prices[J].Resources Policy,69:101829. | |

| Mo D,Gupta R,Li B,al et,2017.The macroeconomic determina-nts of commodity futures volatility:Evidence from Chine-se and Indian markets[J].Economic Modelling,70:543-560. | |

| Owusu O,Wireko I,Mensah A K,al et,2016.The performance of the mining sector in Ghana:A decomposition analysis of the relative contribution of price and output to revenue growth[J]Resources Policy,50:214-223. | |

| Qian Y,Ralescu D A,Zhang B,2019.The analysis of factors affecting global gold price[J].Resources Policy,64:101478. | |

| Raza S A,Shah N,Shahbaz M,al et,2018.Does economic policy uncertainty influence gold prices?Evidence from a nonparametric causality-in-quantiles approach[J].Resources Policy,57:61-68. | |

| Schmidbauer H,Röschc A,2018.The impact of festivities on gold price expectation and volatility[J].International Review of Financial Analysis,58:117-131. | |

| Wang H,Sheng H,Zhang H W,al et,2019.Influence factors of international gold futures price volatility[J].Transactions of Nonferrous Metals Society of China,29(11):2447-2454. | |

| Yang Liuyong,Shi Zhentao,2004.Analysis of long-term determinants of gold price[J].Statistical Research,21(6):21-24. | |

| Yang Shenggang,Chen Shuaili,Wang Dun,2014.Research on influencing factors of gold futures price in China[J].The Theory and Practice of Finance and Economics,35(3):44-48. | |

| Yang Ye,2007.Linkage analysis of gold price and oil price[J].Gold,28(2):4-7. | |

| Yang Zhenguo,Zhang Tong,2009.Analysis of gold market speculation[J].Finance and Accounting Monthly,4(12):41-43. | |

| Zhang Cilan,Huan Hongyan,2009.Empirical analysis of oil price and gold price[J].Southwest Finance,(3):50-51. | |

| Zhang Qidi,2017.Influencing factors and future trend of global gold price[J].South China Finance,(4):74-83. | |

| Zhu X H,Zhang H W,Zhong M R,2017.Volatility prediction of China’s nonferrous metals futures market[J].Transactions of Nonferrous Metals Society of China,27(5):1206-1214. | |

| Zhu Y H,Fan J W,Tucker J,2018.The impact of monetary policy on gold price dynamics[J].Research in International Business and Finance,44:319-331. | |

| Zou Zi’ang,Peng Xiaofan,Pi Jun,2018.Research on hedging ability of international gold spot market—Based on DCC-GARCH model[J].The Theory and Practice of Finance and Economics,39(6):44-50. | |

| 陈艳艳,2018.政治不确定性与企业行为研究述评[J].财会通讯,(6):116-123,129. | |

| 冯辉,张蜀林,2012.国际黄金期货价格决定要素的实证分析[J].中国管理科学,20(增1):424-428. | |

| 冯钰瑶,刘畅,孙晓蕾,2020.不确定性与原油市场的交互影响测度:基于综合集成的多尺度方法论[J].管理评论,32(7):29-40. | |

| 高菲,顾炜宇,2018.“一般商品-保值手段”双重属性视角下的国际黄金价格影响因素研究[J].中国软科学,(5):160-170. | |

| 胡恩同,2005.黄金的双重属性与其价格决定机制[J].黄金科学技术,13(5):1-7. | |

| 华健,刘辰君,2010.从供需角度看黄金价格的变化[J].金融与经济,(12):30-33. | |

| 黄国轩,2019.我国黄金期货市场价格发现功能实证研究[J].价格理论与实践,(9):92-95. | |

| 刘昊然,2007.黄金价格影响因素和投资策略分析[J].价格理论与实践,(10):57-58. | |

| 刘杰,2017.石油与黄金的价格联动分析[J].黄金,38(2):5-7,14. | |

| 刘曙光,胡再勇,2008.黄金价格的长期决定因素稳定性分析[J].世界经济研究,12(2):35-41,87. | |

| 陆国庆,李明雪,2017.美元指数与黄金价格联动性研究[J].价格理论与实践,(5):109-112. | |

| 杨柳勇,史震涛,2004.黄金价格的长期决定因素分析[J].统计研究,21(6):21-24. | |

| 杨胜刚,陈帅立,王盾,2014.中国黄金期货价格影响因素研究[J].财经理论与实践,35(3):44-48. | |

| 杨叶,2007.黄金价格和石油价格的联动分析[J].黄金,28(2):4-7. | |

| 杨振国,张彤,2009.黄金市场投机度分析[J].财会月刊,4(12):41-43. | |

| 张次兰,郇红艳,2009.石油价格与黄金价格的实证分析[J].西南金融,(3):50-51. | |

| 张启迪,2017.全球黄金价格的影响因素及未来趋势[J].南方金融,(4):74-83. | |

| 邹子昂,彭啸帆,皮俊,2018.国际黄金现货市场的避险能力研究——基于DCC-GARCH模型[J].财经理论与实践,39(6):44-50. |

| [1] | 郑明贵,彭群婷,陶思敏,刘丽珍. 经济政策不确定性、投资者情绪与黄金价格波动[J]. 黄金科学技术, 2022, 30(6): 891-900. |

| [2] | 张文伟, 底青云, 雷达, 马凤山. 物探新方法-多通道瞬变电磁法在金属矿勘探中的应用[J]. 黄金科学技术, 2018, 26(1): 1-8. |

|

||

©2018 黄金科学技术编辑部

电话:0931-8277791

E-mail: hjkx@lzb.ac.cn 邮编:730000

甘公网安备 62010202000672号

甘公网安备 62010202000672号